PII redaction in commercial P&C submission intake: the regulatory layer carriers underestimate

.png)

.png)

- Commercial property and casualty submission intake routinely contains personally identifiable information that is governed by overlapping regulatory regimes, including the NAIC Insurance Data Security Model Law, the New York Department of Financial Services Cybersecurity Regulation, the Gramm Leach Bliley Act, and a growing number of state level insurance data security statutes adopted between 2024 and 2026.

- Most carriers focus their data security review on the storage and transmission layer. The exposure that drives regulator action and broker contract disputes sits earlier in the workflow, at the moment a broker submission email reaches the underwriting inbox and is processed by a vendor pipeline.

- A 2026 production grade approach to submission intake treats personally identifiable information as a first class field with a defined retention rule, an auditable redaction step, a documented data residency boundary, and a contractual right to deletion. Vendors that cannot evidence each of these are not operating at a commercial P&C standard.

- The economic exposure is no longer theoretical. Insurance Information Institute and S&P Global outlooks for 2026 both flag cyber and privacy regulation as a rising operational cost line for commercial carriers, and broker confidentiality clauses now routinely require carriers to extend the same protection to any third party processor.

- Pibit.AI is built around a contractual accuracy and contractual security posture. The CURE platform processes broker submissions inside customer controlled cloud regions, applies field level personally identifiable information handling, supports configurable retention policies, and provides full extraction lineage that an auditor or regulator can review.

The hidden middle layer of commercial P&C submission intake

.png)

Every commercial property and casualty submission carries data that is not on the application form but is regulated as if it were. Driver names and dates of birth on a fleet schedule. Workers compensation classification with a key employee's social security number. A loss run referencing a named insured's home address. A broker email forwarding a prior carrier's underwriter notes.

Carriers tend to discuss data security as a perimeter question. The relevant question for submission intake is upstream of the perimeter. It is the question of what a vendor sees, how long the vendor retains it, where the data physically resides while it is being processed, and what evidence the carrier can produce when a state insurance commissioner asks.

This middle layer is where 2026 risk has shifted. Eleven states have adopted some form of the NAIC Insurance Data Security Model Law since 2017, and the model has been updated to track NYDFS Part 500 amendments that took effect in 2024 and 2025. The result is a real obligation on commercial carriers to evidence that any third party with access to non public personal information has a controllable, auditable, and defensible posture across the entire data lifecycle. Submission intake sits at the front of that lifecycle.

The cost of getting this wrong has changed too. The Insurance Information Institute notes that cyber liability and privacy related operating costs are a growing share of the commercial expense ratio. S&P Global's 2026 US property and casualty outlook flags regulatory examination intensity as one of the year's top operational risk lines. Underwriters are no longer the only people in the room when carriers select an intake vendor. Chief information security officers, general counsel, and chief risk officers now read the same evaluation packet.

The four obligations every submission intake vendor must satisfy

A 2026 commercial P&C carrier should expect any vendor processing broker submissions to evidence four obligations in writing, with operational artefacts that an auditor can inspect.

Obligation 1: Field level personally identifiable information handling

Personally identifiable information is not a single class. A driver licence number is a high risk identifier. A named insured's business address is lower risk. A producer code is generally not personally identifiable information at all. A production grade vendor distinguishes these classes at the field level and applies different policies to each.

What a carrier should expect to see is a written taxonomy that maps every field the vendor extracts to a class, with a default retention rule per class, a default redaction rule for downstream display, and a default access control list. Storage encryption at rest is the floor, not the ceiling.

Obligation 2: Data residency and processing locality

A broker email arriving at a US commercial carrier may be processed in a cloud region the carrier never explicitly selected. A vendor that runs extraction inside its own multi tenant cluster, in an undisclosed region, with model providers in a third location, is not operating at the commercial P&C standard.

The 2026 standard is that the carrier specifies the cloud region and account, that processing occurs inside that region, and that no broker submission data leaves the region for any reason without an explicit, contractual basis. This is now a regulatory expectation in any state that has adopted the NAIC Model Law and a contractual expectation in most large brokerage agreements.

Obligation 3: Retention, deletion, and the right to be forgotten

A carrier should not retain a broker submission longer than the underwriting and audit cycle requires. A vendor should not retain it at all unless the carrier has explicitly authorised it.

Operationally, this means that the vendor pipeline must be able to delete a submission, and every artefact derived from it, on demand. Evidence of deletion, with a cryptographic or system level attestation, is not a luxury. It is a control that an examiner will ask for. Vendors that store extraction outputs indefinitely for model improvement, without an opt out, are not in step with 2026 expectations.

Obligation 4: Lineage and explainability

Every extracted field should carry lineage back to its source document, page, and bounding region. Every transformation, normalisation, and quality check should be timestamped and recorded. Every human review action should be logged.

This is not only a compliance requirement. It is also a quality requirement. The same lineage that allows a regulator to audit a privacy event allows a commercial underwriter to defend a quote against a broker dispute. A vendor that cannot produce field level lineage on demand is asking the carrier to absorb both risks.

Why the redaction problem is structurally harder in commercial P&C

Personal lines carriers have spent a decade refining personally identifiable information handling for a constrained, well structured submission flow. Commercial property and casualty has none of those constraints.

The submission intake universe in commercial P&C contains hundreds of broker formats, dozens of document classes from ACORD applications and statements of values to driver schedules and prior loss runs, free text email bodies that may include personal information not on any form, and a forwarded thread history that often quotes prior submissions. A field level redaction system has to identify personally identifiable information across every one of those surfaces, in every one of those formats, with no false negatives on the high risk classes and no false positives that strip a valid underwriting field.

The combinatorial problem is why template based optical character recognition pipelines fail. The format universe is too wide for any template library to cover. It is also why generic large language model approaches do not satisfy the obligation. A general purpose model can read a broker email fluently. It cannot guarantee that every social security number in every loss run referenced in every forwarded thread has been classified, masked at the right layer, and logged with field level provenance.

The production grade architecture for commercial P&C submission intake therefore has three layers that operate together. The first layer is a specialised extraction stack tuned per document class, with personally identifiable information taxonomy built into the extraction step itself rather than added afterwards. The second layer is an agentic quality assurance step that cross checks personally identifiable information across the email body, the attachment set, and the forwarded thread, and resolves contradictions before the data reaches the underwriter. The third layer is human expert review for high stakes fields, with a closed loop that adjusts the extraction stack against any field error.

For a deeper view of why the submission intake architecture has to be multi layered, see submission turnaround time in commercial P&C and why a 95 percent extraction accuracy headline is not production accuracy.

How the regulatory layer translates into a 2026 evaluation rubric

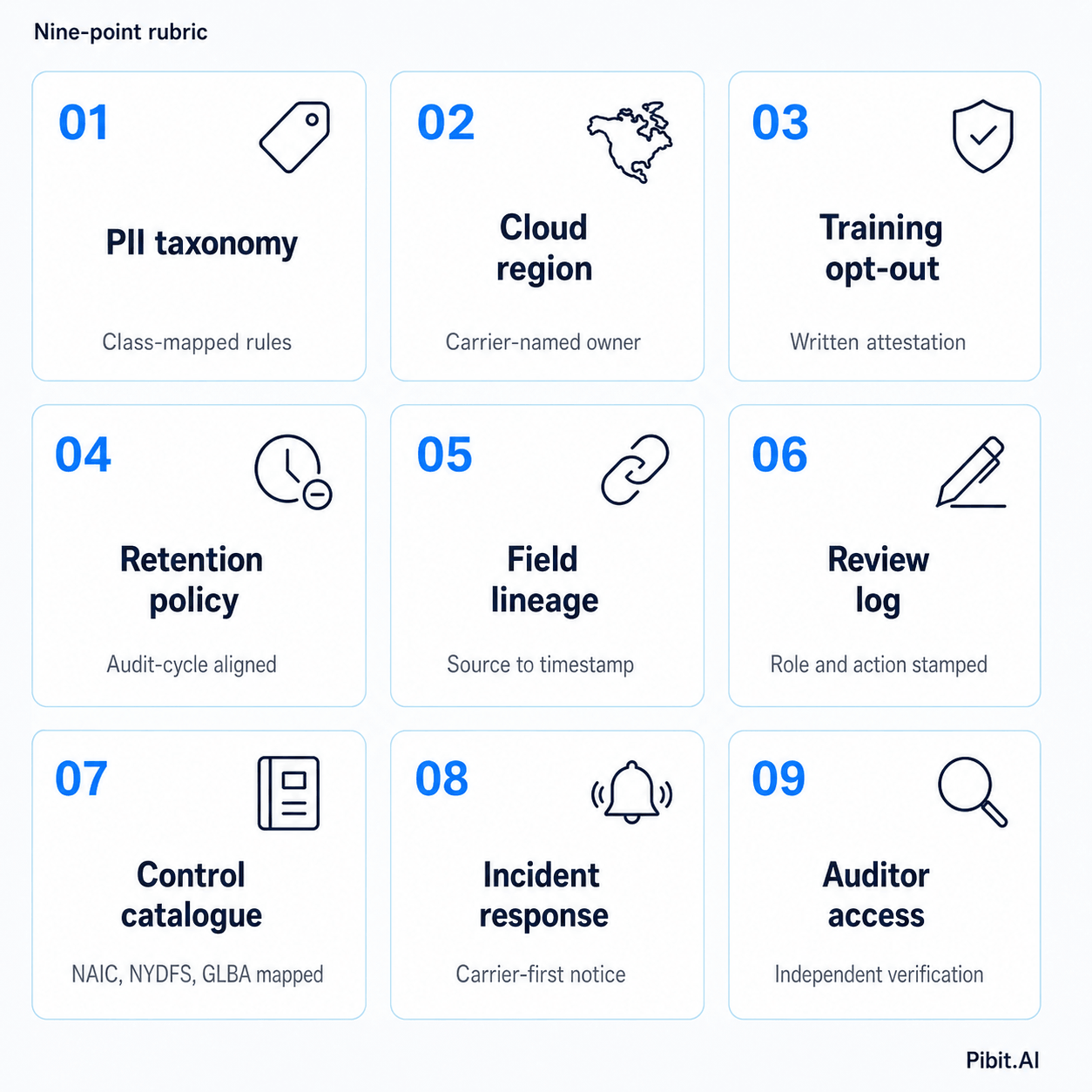

A chief information security officer evaluating a submission intake vendor in 2026 should expect to score the vendor across nine specific evidence requirements. None of these are theoretical. Each maps to a regulator question or a broker contract clause.

- A written taxonomy of personally identifiable information classes, with retention and redaction rules per class.

- A description of the cloud region and account model, with the carrier as the named region owner.

- A written attestation that broker submission data is not used to train models that serve other carriers, unless the carrier has explicitly contracted to allow it.

- A documented retention policy with a default not to exceed the carrier's underwriting and audit cycle, with an explicit deletion mechanism the carrier can invoke at any time.

- Field level lineage on every extracted value, with source document, page, region, and timestamp.

- A logged human review record on every high risk field, with the reviewer's role and the action taken.

- A documented control catalogue mapped to NAIC Model Law sections, NYDFS Part 500 obligations where applicable, and GLBA safeguards rule expectations.

- An incident response procedure that includes carrier notification within a defined service level, ahead of the regulatory notification window.

- An auditor's access pattern that allows independent verification of all of the above without depending on vendor provided dashboards.

A vendor that cannot produce written evidence against each of these in a single procurement cycle is not operating at the commercial P&C standard. A vendor that can produce all nine within a procurement cycle is rare, and is the standard a CISO and a chief underwriting officer should hold their procurement team to.

For carriers building this rubric internally, the data security checklist for AI underwriting vendors provides a more granular operational walk through. For carriers building the broader vendor governance program, the agentic AI architecture in underwriting explains why a multi layer pipeline is required to evidence any of these obligations at scale.

What the unit economics look like for a $500 million GWP carrier

The cost of getting submission intake personally identifiable information handling wrong is not abstract. For a hypothetical $500 million GWP commercial carrier processing 35,000 submissions a year, three exposure lines apply.

The first is the regulatory examination cost. A state insurance commissioner examination triggered by a notification event under NAIC Model Law typically consumes between 250 and 600 internal personnel hours and an external counsel engagement that runs into the low six figures. A vendor that cannot produce field level lineage and a documented control catalogue forces the carrier to absorb the entire data production burden internally.

The second is broker contract exposure. Commercial brokerage agreements increasingly include a flow down clause that requires the carrier to extend the same data handling obligations to any third party. A vendor that retains submission data indefinitely, that cannot evidence deletion, or that processes outside the carrier's specified region, is a flow down clause violation in waiting. The legal cost of one mid sized broker dispute on this question is comparable to a year of premium on the relationship.

The third is reputational exposure. Brokers route submissions to the carriers they trust. A single broker side notification event involving a vendor in the carrier's intake stack reduces submission volume from that broker for the following renewal cycle, often by twenty to forty percent based on retention and re submission patterns. On a ten percent quote ratio and a thirty percent bind ratio, a single event removes a measurable share of forward year premium.

The combined exposure on these three lines is meaningful enough that the chief financial officer is now part of the vendor selection conversation. The carriers that get this right treat personally identifiable information handling in submission intake as a margin item, not a hygiene item.

What Pibit.AI does differently

Pibit.AI was designed for commercial P&C submission intake specifically, and the platform's data security posture reflects that. Three properties matter.

First, the CURE platform processes broker submissions inside customer controlled cloud regions. The carrier names the region. The carrier owns the account. No broker submission data crosses the boundary unless the carrier has explicitly authorised it.

Second, personally identifiable information handling is built into the extraction pipeline, not applied afterwards. The taxonomy is field level. The redaction rules are configurable per carrier and per document class. The retention policy is configurable, with deletion attestations on demand.

Third, every extracted field carries lineage back to the source document, page, and region. Every transformation is timestamped. Every human review action is logged. The same provenance that defends accuracy against a broker dispute defends privacy against a regulator question.

The result for a Pibit.AI carrier is a submission intake stack that an auditor, a regulator, a broker, and an underwriter all view through the same evidence base. The economic effect is measurable. Pibit.AI customers reduce submission turnaround time by 85 percent, grow gross written premium per underwriter by approximately 32 percent, and recover meaningful loss ratio because the data quality is set the moment the email is read. The privacy and security posture is what makes that operational lift defensible at the board level.

The next twelve months

The regulatory direction of travel through the end of 2026 is more disclosure, more documentation, and more carrier accountability for vendor behaviour. The NAIC Model Law will continue to be adopted in new states. NYDFS Part 500 amendments will continue to set the floor for what other regulators expect. State level insurance data security statutes that have been introduced but not yet adopted are expected to move through legislatures in 2026 and 2027.

The carriers that prepare for this trajectory now, by holding their submission intake vendors to a written evidence base across the four obligations and the nine evaluation requirements, will spend 2026 underwriting more confidently and more profitably. The carriers that wait will spend 2026 explaining themselves to examiners.

Frequently Asked Questions

Commercial property and casualty submissions routinely contain driver names and dates of birth on fleet schedules, key employee identifiers on workers compensation classifications, named insured business and home addresses on application forms, and free text personal information in broker email bodies and forwarded threads. They also contain producer level personal data on broker emails and signatures. Each class carries a different regulatory weight, and a production grade intake vendor classifies them at the field level rather than treating personally identifiable information as a single category.

The NAIC Model Law, adopted in some form by eleven states as of 2026, requires licensed insurers to implement an information security program that addresses third party processors with the same rigour as internal systems. For submission intake, this means a carrier must be able to produce written evidence that any vendor processing broker submission data has a documented control catalogue, a retention policy aligned with the carrier's audit cycle, a defined data residency boundary, and an incident response process that meets carrier notification timelines. A vendor that cannot evidence these in a procurement cycle is a regulatory exposure, not just an operational risk.

A vendor data security claim is a marketing artefact. Production grade evidence is a procurement artefact. A claim says the vendor encrypts data at rest. Evidence is a written taxonomy of personally identifiable information classes mapped to retention rules, a named cloud region with the carrier as account owner, a deletion attestation pattern that an auditor can inspect, field level lineage on every extracted value, and a control catalogue mapped to specific regulatory sections. The 2026 commercial P&C standard is that vendors produce evidence on demand, not claims on a website.

Underwriting Assistant

.png)

.png)

Ready to optimize