E&S submission volume is rising while rates soften: why surplus lines growth is now a throughput problem

.png)

- US surplus lines direct premium written reached an estimated $82 billion in 2025, up from under $18 billion in 2015, but growth slowed to 9.7 percent through Q3 2025 from 13.5 percent a year earlier.

- AM Best revised the E&S segment outlook from positive to stable in November 2025, citing moderating premium growth and early rate softening in property, cyber, and D&O.

- Submission volume into the wholesale channel has not slowed, so the operational bottleneck is now throughput, not pricing.

- When rate stops doing the work, margin is decided at intake: how fast a carrier clears, prioritizes, and quotes the accounts worth winning.

- Surplus lines submissions are the hardest in commercial P&C to process manually, which is why intake automation, not more headcount, is the realistic path to capacity.

For seven years, the excess and surplus lines market grew on a simple tailwind. Admitted carriers retrenched, hard-to-place risk flowed into the surplus lines channel, and rate kept climbing. Direct premium written by US surplus lines insurers went from just under $18 billion in 2015 to roughly $82 billion in 2025, with double-digit growth nearly every year along the way. Growth was something the market caught, not something it had to engineer.

That phase is closing. AM Best moderated its read on the segment in November 2025, revising the E&S outlook from positive to stable. Premium growth slowed to 9.7 percent through the first nine months of 2025, down from 13.5 percent in the same period a year earlier. Property, cyber, and directors and officers liability all showed early signs of rate softening. And yet submissions kept flowing into the wholesale channel at full volume.

That combination is the part most growth plans have not absorbed yet. The risks are still arriving. The pricing power that used to convert them into margin is thinning. When a carrier can no longer rely on rate to manufacture profit, the next lever is the one most surplus lines operations have neglected for a decade: how much of the incoming submission flow they can actually evaluate, price, and quote well, fast enough to win the accounts worth winning.

The growth story the numbers no longer tell

The surplus lines expansion of the last decade was real, and it was structural. Catastrophe-exposed property, complex casualty, emerging cyber exposures, and risks that admitted markets would not write all found a home in E&S. The freedom of rate and form that defines the surplus lines market let carriers price uncertainty that standard markets could not. For most of that run, the binding constraint was appetite, not capacity. If you wanted to grow, you opened your appetite, and the premium followed.

The 2025 data complicates that reflex. Property is softening as reinsurance capital returns and the 2025 hurricane season stayed relatively quiet. Cyber has been declining for several quarters as capacity remains abundant and buyers with strong controls negotiate better terms. D&O continues to drift down. These are exactly the lines that powered a meaningful share of the E&S surge, and they are the ones where pricing is now working against the carrier rather than for it.

The casualty side tells a different story, and it matters for how throughput pressure shows up. General liability, commercial auto, and excess and umbrella remain firm to hard, pushed by social inflation, nuclear verdicts, and litigation funding that now sits on more than $16 billion in assets. So the typical E&S book in 2026 is carrying two opposite dynamics at once: lines where you cannot raise rate, and lines where you must underwrite far more carefully because a single misjudged account can move loss ratios for years. Both pressures land on the same operational surface. Both are decided in the first hours after a submission arrives.

Why throughput is the lever, not appetite

Consider what actually happens when an E&S carrier decides to grow in a softening rate environment. It cannot lift rate to expand the top line, because the market will not bear it. It can broaden appetite, but broader appetite means more submissions, more documents, and more marginal accounts that demand judgment rather than rote processing. It can hire underwriters, but skilled surplus lines underwriting talent is scarce and expensive, and headcount scales linearly while submission volume scales faster.

The result is a quiet capacity ceiling. Underwriting teams already report that the sheer volume of incoming submissions, combined with talent shortages and the heightened scrutiny each account now requires, is straining both people and workflow systems. When every submission takes 30 to 60 minutes of manual assembly before an underwriter can even begin to evaluate the risk, the math is unforgiving. A team that can touch 200 submissions a week cannot suddenly touch 300 because leadership decided to grow. Something gives, and what usually gives is selection quality, broker responsiveness, or both.

This is the core shift. In a hard market, the carrier that quotes fastest often wins because brokers place with whoever responds first on an account everyone wants. In a softening market, the carrier that quotes fastest on the right accounts wins, because margin now depends on selecting well across a larger flow, not pricing high on a smaller one. We have written before about how submission speed becomes a margin problem once rate relief disappears. In E&S, that problem is amplified by the nature of the submissions themselves.

The surplus lines submission is the hardest in commercial P&C

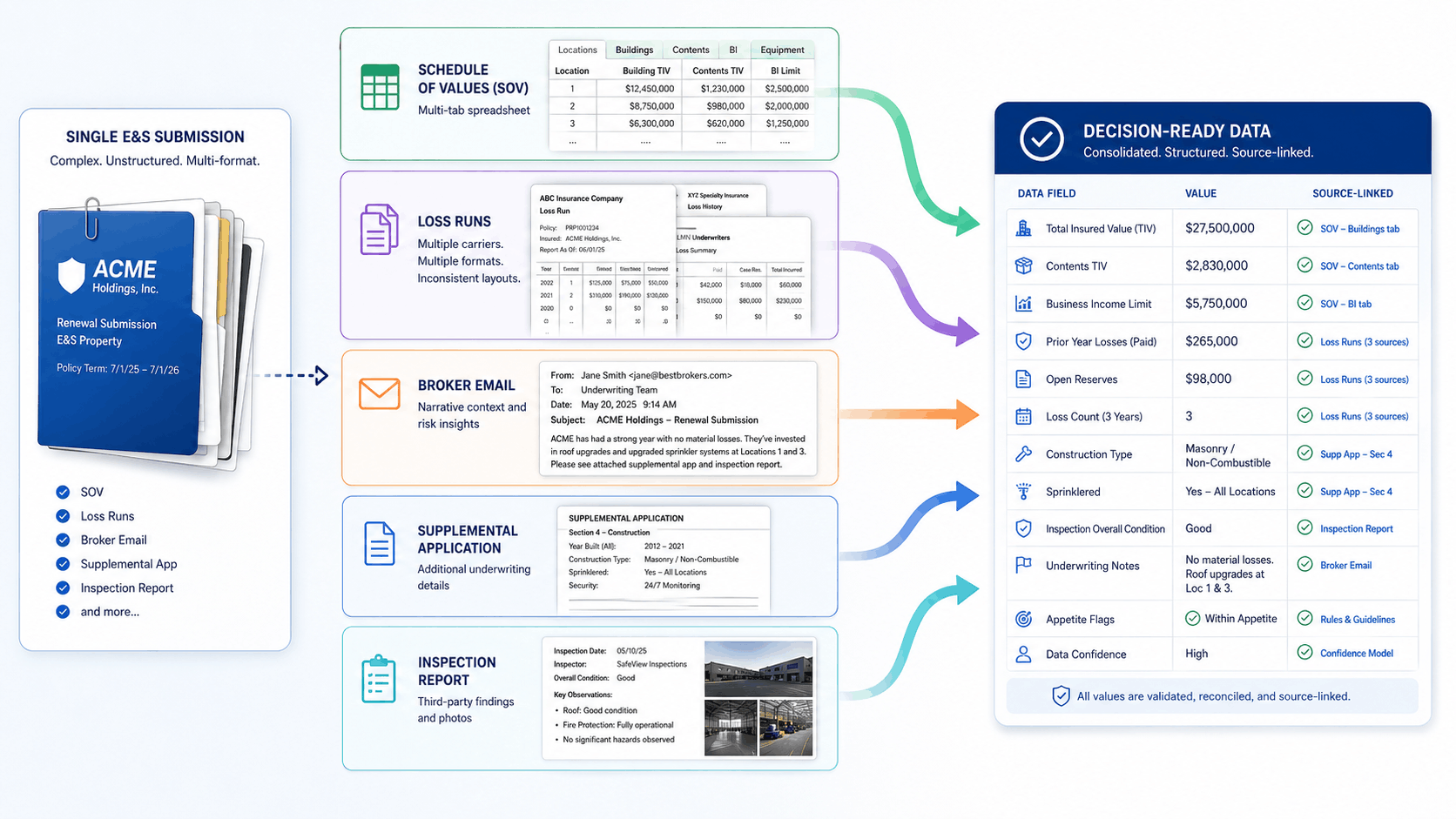

There is a reason intake automation matters more in E&S than almost anywhere else in commercial insurance. Surplus lines submissions are, by definition, the messy ones. They arrive through the wholesale channel, often touched by multiple intermediaries, in formats no two brokers structure the same way. A single account can carry a 200-tab statement of values, loss runs spanning several prior carriers in incompatible layouts, narrative broker emails that contain the actual risk story, supplemental applications, and inspection reports. The unstructured, multi-source nature of the submission is precisely what makes the risk worth E&S pricing, and precisely what makes it slow to process.

Manual handling of these submissions creates three compounding costs. The first is cycle time. Hours spent assembling and rekeying data are hours not spent on risk evaluation, and they delay the quote past the point where a broker has already placed elsewhere. The second is selection error. When data is rekeyed under time pressure across dozens of inconsistent documents, a wrong total insured value or a missed loss in the run can mean a mispriced account that erodes margin for the life of the policy. In a market where rate no longer covers underwriting mistakes, that error is more expensive than it used to be. The third is the opportunity cost of capacity: every submission stuck in clerical processing is throughput the carrier paid for and did not use.

Generic optical character recognition does not solve this, because surplus lines document variety breaks template-trained tools. The moment a new broker format or a non-standard loss run layout appears, accuracy degrades, and underwriters stop trusting the output. A tool no one trusts is worse than no tool, because the team works around it while the carrier still pays for it. This is the failure pattern we examined in why AI alone will not fix submission intake, and it is sharpest in exactly the high-variation environment that defines E&S.

What growth through throughput looks like operationally

The carriers positioning well for the next phase of the surplus lines market are treating intake as a capacity decision, not an IT project. The objective is straightforward to state and hard to execute: process more of the incoming submission flow, with verified accuracy, fast enough that underwriters spend their hours on judgment rather than data entry.

Three operational moves define that posture.

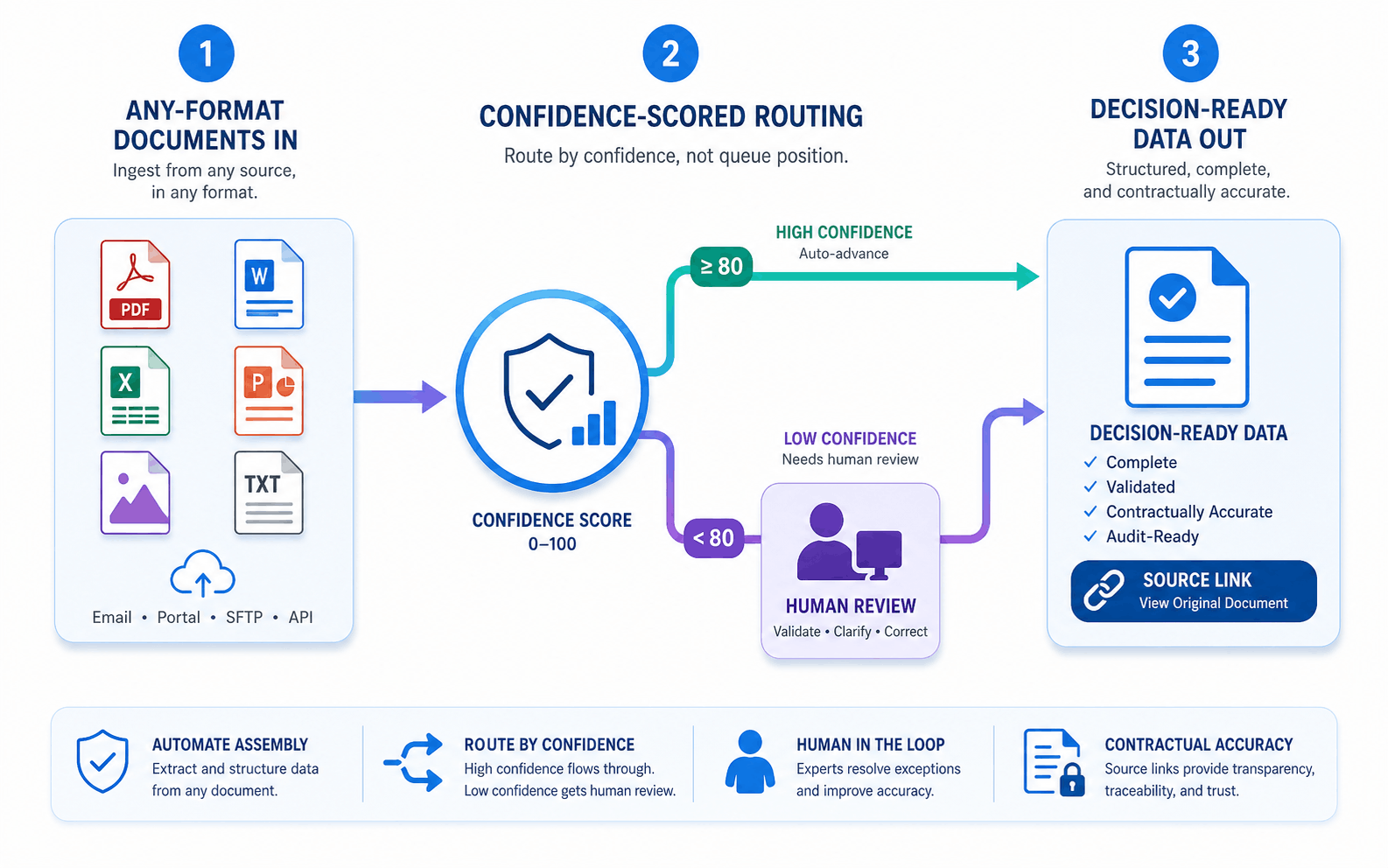

First, automate the data assembly, not the decision. Template-agnostic extraction pulls structured, rater-ready data from any broker's format without per-format training, so the variety that defines E&S stops being a bottleneck. The underwriter receives decision-ready data instead of a folder of PDFs, and the human judgment that surplus lines pricing depends on is preserved, not replaced. This is the Centaur Underwriter model: the expert augmented, handling more volume without lowering the bar on selection.

Second, route by confidence, not by queue position. Most surplus lines operations still process submissions first in, first out, which means a marginal account and a clean, in-appetite account get the same wait. Confidence scoring lets low-confidence extractions route to human review while high-confidence data flows straight through, so underwriting attention concentrates where it changes the outcome. The carrier clears the easy accounts in minutes and reserves its scarce expert hours for the complex ones that justify E&S pricing.

Third, make accuracy contractual, not aspirational. In a softening market the cost of a mispriced account is no longer absorbed by rate, so the data underneath every quote has to be verifiable. A three-layer model of AI extraction, agentic quality assurance, and human expert review delivers accuracy the carrier can defend, with every data point linked back to its source document. When an account goes sideways two years later, the file shows exactly where each number came from.

The carriers that build this capacity do not just survive the softening. They use it to take share, because they can say yes to more of the flow than competitors stuck at a manual capacity ceiling. We have made the broader version of this argument in the operational case for underwriting automation when rates soften, and the E&S segment is where the case is most acute, because the submissions are hardest and the margin for error is thinnest.

The decision in front of E&S leadership

The surplus lines market is not contracting. AM Best expects premium to flatten in the near term while the segment continues to absorb a growing number of risks better suited to E&S than to admitted markets. The flow is still there. What has changed is that the flow no longer converts itself into margin through rate. It has to be converted through operations: clearing more of it, selecting better within it, and quoting it before the broker places elsewhere.

That reframes a question many E&S carriers and MGAs have been deferring. The question is not whether to automate submission intake. It is whether the organization can grow GWP without growing headcount in a market that no longer rewards raising rate. For most surplus lines operations running manual or offshore intake today, the honest answer is that they cannot, not at the volume the next phase of growth requires. The carriers that resolve that constraint first will define the winners of the post-tailwind E&S market.

The surplus lines market still has the flow. The advantage now goes to carriers that can convert more of it without adding headcount. See how the CURE™ platform turns variable, multi-source surplus lines submissions into decision-ready data with verified accuracy.

Frequently Asked Questions

Premium growth and submission volume are different things. Growth slowed to 9.7 percent through Q3 2025 mainly because rates softened in property, cyber, and D&O, which lowers premium per account. But admitted carriers continue to push hard-to-place risk into the wholesale channel, so the number of submissions arriving stays high even as the dollar growth per submission shrinks. That gap is exactly what creates throughput pressure.

When rate is firm, higher pricing can absorb a mispriced or slowly quoted account. When rate softens, that cushion disappears, so margin depends on selecting well across a larger flow and quoting fast enough to win the right accounts. Operationally, that shifts the priority from raising rate to increasing throughput and accuracy at submission intake, where speed and selection are actually decided.

Surplus lines submissions arrive in highly variable formats through the wholesale channel, with documents like multi-tab statements of values, loss runs from several prior carriers, and narrative broker emails. Template-trained OCR breaks when formats drift, degrading accuracy and trust. Template-agnostic extraction, paired with human expert review, handles that variation reliably, which is why intake automation built for underwriting outperforms generic document tools in E&S.

Senior Underwriting Operations

.png)

.png)

Ready to optimize