The underwriting reorg: A human's guide to who survives the AI shift in commercial insurance

.png)

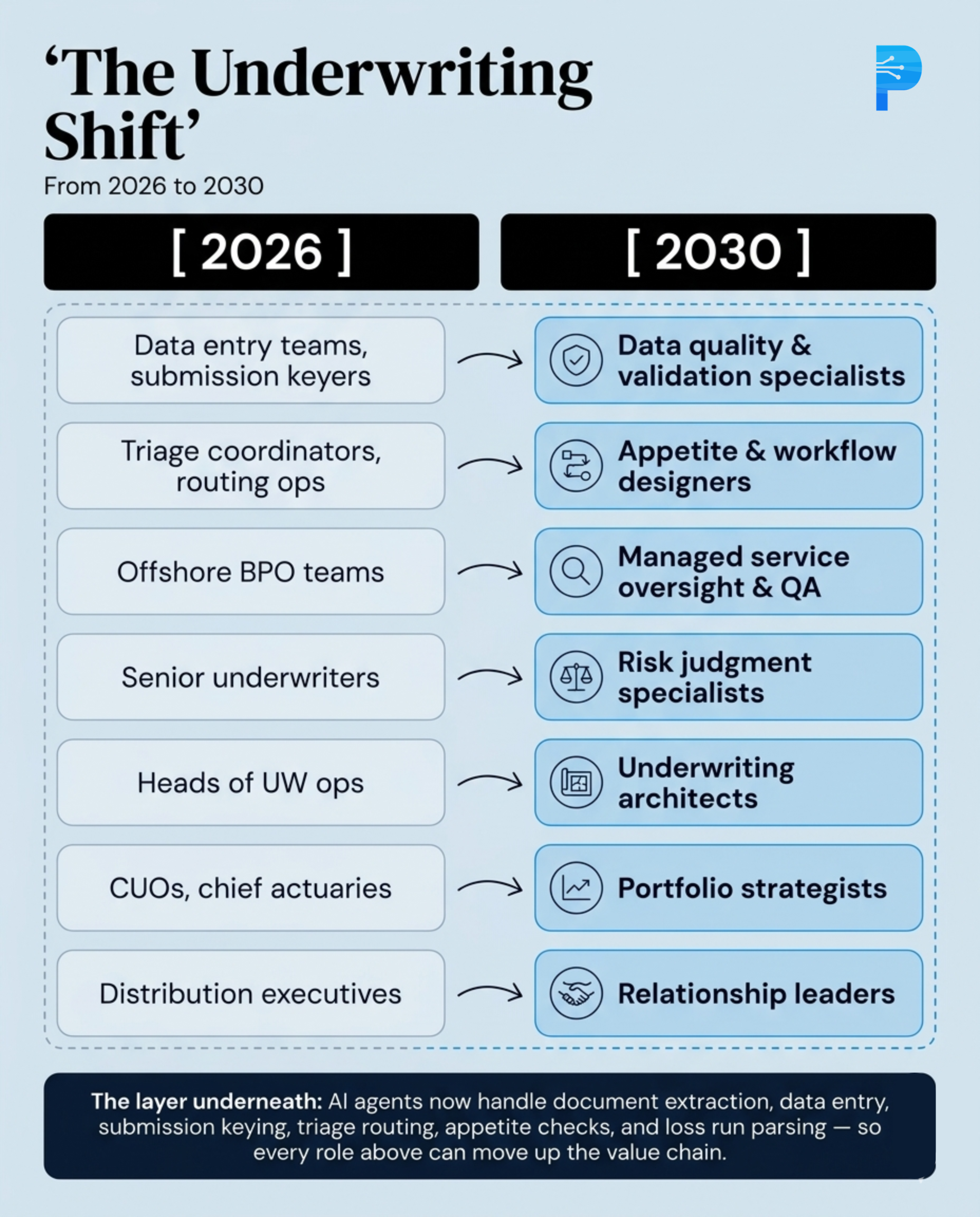

- The underwriting org chart is being redrawn. Pre-decision admin work, data entry, triage, offshore processing, enrichment research, is moving to AI agents.

- What survives is judgment, architecture, accountability, and trust.

- Four roles become more valuable than ever: risk judgment specialists, underwriting architects, portfolio strategists, and distribution relationship leaders.

I have spent the last 18 months in conversations with over 100 underwriting leaders at carriers, MGAs, and mutuals. Most of them are asking which roles survive when AI handles the work those roles were created to do.

One carrier hired a 4-person team last quarter just to handle submission triage. That team's entire function, sorting which submissions deserve underwriter attention and which do not, is something a structured intake system does in seconds. Another carrier has an offshore processing team that takes 24 hours for basic submission setup. A third runs triple data entry across three separate systems before an underwriter can start evaluating risk.

Cases like these are the standard operating model at most commercial carriers today. And there is a high chance that every one of these workflows will look unrecognizable by 2030.

In 5 years, every carrier and MGA will have fewer people processing submissions. Not because of layoffs. Because the work itself will no longer exist.

The red zone: Tasks that AI agents replace

Let me be specific about what is going away. Not "some jobs." These jobs.

Submission intake clerks and data entry specialists

Today, someone opens an email, downloads a PDF, identifies the line of business, and logs it into a CRM. Then someone else extracts data from loss runs, applications, and supplements and re-keys it into a policy admin system.

At one carrier we work with, underwriters were doing triple data entry across a policy administration platform, a CRM, and a document management system before they could start any risk evaluation. API response times between those systems ran 20 to 25 seconds per call.

AI agents handle this end-to-end. Document classification identifies every incoming file type. Template-agnostic extraction pulls structured data from any format. The system of record gets populated automatically.

The data: 50%+ of underwriter time today is consumed by pre-decision administration (Accenture/The Institutes 2021, corroborated by Capgemini 2024). That percentage goes to near-zero.

Offshore BPO processing teams

The service model in insurance is human plus time. You pay for headcount. Ten people processing submissions at $40 per hour. It is expensive, slow, and it scales linearly with volume.

One MGA we spoke with has an offshore team that takes 24 hours just for basic submission setup. Then hours of additional data entry before any underwriting begins. Their end-to-end cycle is 48+ hours.

AI-enabled services replace the entire labor arbitrage model. Not with a product the carrier has to learn and configure, but with an outcome: processed, decision-ready submissions delivered before the underwriter opens the file.

The data: At current offshore rates, a carrier processing 10,000 submissions a year spends roughly $750K to $1.2M on manual intake labor annually. The AI-enabled service model delivers the same output at a fraction of the cost and a fraction of the time.

Triage coordination and basic clearance checking

A carrier processing 20,000 submissions a year quotes 2,000. That is a 13% quote rate. The other 87% consumed underwriter time and produced nothing.

Most of those 87% should never have reached an underwriter. They were outside appetite, incomplete, duplicates, or wrong LOB. But without structured triage, someone had to open every single one and make that determination manually.

AI handles appetite validation, duplicate detection, and completeness scoring simultaneously. The 87% gets filtered before it wastes a single minute of underwriter judgment.

The data: 30% of submissions reaching underwriters are outside appetite (estimated across 40+ carrier conversations in Q1 2026). At 50 underwriters, 2 hours per file, and $75/hour, that is $1.4M per year in wasted judgment capacity.

Junior analysts doing enrichment research

An underwriter evaluating a professional liability submission for a CPA firm needs to check state license boards across every state the firm operates in, pull PCAOB audit history, check SEC filings for 'going concern' flags, and screen principals against OFAC sanctions lists.

That research used to take hours for a single firm. For complex firms with multiple offices and public audit clients, it could take half a day.

Automated web enrichment does all of this before the file is opened.

The data: We expanded from a single-state pilot to all 50 states at go-live for one carrier. The enrichment that took an analyst 4+ hours now takes minutes and covers sources the analyst would not have checked.

The green zone: 4 roles that not only survive but become more valuable

Here is the part that matters: AI does not eliminate underwriting. It eliminates the logistics around underwriting. The roles that survive are the ones that require judgment, accountability, architecture, and trust.

1. Risk judgment specialists (human validators)

Who they are today: Underwriters and specialized risk assessors.

What changes: Their time allocation flips. Today, a senior underwriter spends 60% of her day on administration (data assembly, document review, CRM logging, broker chasing) and 40% on actual risk judgment. By 2030, that ratio inverts. 10% administration. 90% judgment.

When an AI system presents a submission with 80+ risk factors already scored, positive and negative signals organized, third-party data enriched and sourced, the underwriter's job becomes: do I agree with this assessment, and what does my experience tell me that the model does not know?

This is the centaur underwriter, and not a human replaced by AI. A human expert whose judgment is compounded by a system that surfaces what she would have found eventually, but faster and with sources cited.

How it works in practice: At one carrier we are deploying with, underwriters give structured feedback when they disagree with a score. Thumbs up or down with a description of what was missed or misweighted. The model learns from described disagreement and the underwriter teaches the system. The system makes the underwriter faster. The loop compounds.

The metric that proves it: 32% more GWP per underwriter when judgment time is protected from administrative interruption.

2. Underwriting architects (system architects)

Who they are today: Heads of Underwriting Operations, Directors of Process Excellence, Underwriting Technology Leads.

What changes: This becomes the highest-leverage role in the entire organization.

Today, these people manage workflows. They oversee triage queues, design referral guidelines, maintain underwriting authorities, and handle exception routing. Most of their time is spent keeping the current process from breaking.

By 2030, their job is designing how AI agents and human underwriters work together. They will answer questions like what gets auto-declined, what gets fast-tracked, what triggers a senior underwriter review, what risk factor weights need adjustment based on aggregated feedback, and what the scoring model prioritizes for this specific book, in this specific market, for this specific LOB.

How it works in practice: At one professional liability carrier going live this month, the Head of Underwriting Operations is personally calibrating 80+ risk factor weights in the scoring model. She is deciding which factors penalize an applicant, which ones flag for human review, and which ones are informational only. She designed the rule that absence of information is flagged but not penalized, because penalizing missing data would create false negatives.

These are architectural decisions that define how the entire underwriting operation behaves. Undeniably, they require deep domain expertise combined with systems thinking.

Why it matters: The carrier that designs the best human-AI architecture will underwrite the best book. This is portfolio management disguised as an operations role.

3. Portfolio strategists (chief accountability officers)

Who they are today: Chief Underwriting Officers, Chief Actuaries, CFOs responsible for underwriting P&L.

What changes: Their accountability scope expands, but their decision quality improves dramatically.

Today, a CUO manages combined ratios based on data that is 12 to 18 months old. Loss ratio surprises arrive as quarterly reports, not real-time signals. Portfolio concentration risks are discovered in annual reviews, not daily intake patterns.

By 2030, a CUO would have access to real-time portfolio intelligence derived from every submission processed.

How it works in practice: One carrier's compliance officer asked us: can you show auditors that the scoring model does not discriminate against protected classes? Every factor weight, every variable, every model version is stored and traceable. Data lineage by source (application document, web scraping, government database, third-party enrichment) is available at every submission level.

This is what accountability looks like in an AI-augmented operation. Not trusting a black box, but rather tracing every decision to its data, its model, and its human validator.

The metric that proves it: 700 basis points of loss ratio improvement on a $500M book. That is $35M in improved underwriting margin. Someone has to own that outcome.

4. Distribution relationship leaders (relationship experts)

Who they are today: Broker relationship managers, distribution executives, agency development officers.

What changes: As the operational friction between carriers and brokers decreases, the relationship layer becomes even more important.

78% of brokers say insurer technology strongly influences placement decisions (CIAB 2024). When a broker can submit to a carrier and get a response in 2 hours instead of 48 hours, they send more business. But technology alone does not build loyalty, relationships do.

How it works in practice: At one MGA, the EVP built a rush email workflow specifically for large accounts so underwriters could prequalify them before the standard queue. That is a relationship-driven exception to a technology-driven process. The AI handles the standard flow. The relationship leader handles the exceptions that build trust.

Why it matters: The carriers with the fastest turnaround will attract the most broker flow. But the carriers with the strongest relationships will retain it. Speed is table stakes. Trust is the moat.

Where this is already happening

The reorg is underway at carriers today, whether they call it that or not.

A workers compensation carrier launched AI-assisted intake and went from processing 6 submissions a day to 20. They did not hire 3x the staff. They redeployed existing staff from data entry to risk judgment.

A professional liability carrier that went live with us last month will process 6,000 to 7,000 submissions a year through a structured AI workbench. Their underwriters will stop doing triple data entry and start doing risk evaluation. The 4 to 6 people who were manually assembling context for every account will be redeployed or not replaced when they move on.

An MGA processed 626 submissions last quarter with zero dollar errors. Their submission intake team is not a team anymore: it is a system.

The uncomfortable math

Here is the part nobody wants to say out loud.

A carrier with 50 underwriters, fully loaded at $75,000 each, spends $3.75 million annually on underwriting payroll. If 50%+ of each underwriter's time is spent on pre-decision administration, roughly $1.9 million of that payroll is spent on work that AI agents do better, faster, and cheaper.

The question is not whether to reduce that number. The question is what happens with the capacity you free up. Do you process more submissions with the same team? Do you enter new LOBs? Do you improve your combined ratio by giving underwriters more time for risk judgment?

The carriers that answer that question strategically will outperform. The ones that ignore it will watch their competitors do it first.

The 4 traits that separate who thrives from who does not

Across every deployment I have seen, the underwriting professionals who thrive in the AI-augmented model share four traits:

1. Domain depth over process speed. The people who survive are not the fastest processors. They are the ones who understand the risk at a level the model cannot yet match, like deep LOB expertise, pattern recognition from years of adverse selection, and the ability to see what is not in the submission.

2. Systems thinking. The ability to see how a change in one part of the workflow affects everything downstream. If you adjust a risk factor weight, what happens to your quote rate? If you auto-decline a class code, what happens to your broker relationships? These are architectural questions that require human judgment.

3. Teaching instinct. The most valuable underwriters are the ones who can articulate why they disagree with a model. Not "this score feels wrong" but "this score underweights concentration risk in the audit client portfolio because three of the top five clients are in the same vertical." That is described disagreement through which the model learns.

4. Comfort with accountability. When the AI handles the extraction, enrichment, and scoring, the human is left with the decision. You either make the call, document your reasoning, and own the outcome, or you do not.

The org chart is being redrawn

This is not a future prediction.

Submission intake is becoming automated and data entry is becoming extraction. Enrichment research is becoming web scraping and triaging is becoming intelligent routing. And the underwriter is becoming what they were always supposed to be: a risk judgment specialist.

The carriers that see this now will compound. The rest will wonder what changed.

If you run an underwriting operation with more than 5,000 submissions a year, the reorg is coming to your org chart. The question is whether you design it or whether it happens to you.

Akash is the founder and CEO of Pibit.AI, the AI-native underwriting platform used by 40+ carriers and MGAs. CURE (Centralized Underwriting Risk Environment) handles submission intake, extraction, enrichment, scoring, and routing so underwriters can focus on what they were hired to do: judge risk.

Frequently Asked Questions

No. AI is not replacing commercial underwriters by 2030. It is replacing the administrative work that surrounds underwriting, not the judgment that sits at the center of it.

The work that is moving to AI agents is pre-decision administration: document classification, data entry across multiple rater and policy admin systems, appetite checks, triage routing, duplicate detection, loss run parsing, and enrichment research across state license boards, PCAOB, SEC, and OFAC. That is the work underwriters complain about, not the work they went to school for.

What survives and compounds in value is everything AI cannot do well: pricing a hard risk where the data disagrees with itself, reading a broker relationship, defending a decision to a reinsurance partner, structuring a layered program, and owning portfolio accountability when loss ratios move.

By 2030, senior underwriters at AI-augmented carriers are expected to spend roughly 90 percent of their time on risk judgment and 10 percent on administration. Today the split is closer to 50/50, with more than half of underwriter time consumed by pre-decision admin.

The reorg is not humans out, AI in. It is humans moving up the value chain while AI takes the floor of repetitive work underneath them.

More than 50 percent of a commercial underwriter's day is consumed by pre-decision administration, according to published research from Accenture, The Institutes, and Capgemini.

In practice, that includes:

- Reviewing submission documents across ACORD forms, SOVs, loss runs, and broker emails

- Re-keying data into rating engines and policy admin systems

- Validating whether a risk fits appetite

- Detecting duplicate submissions across channels

- Parsing loss runs into structured tables

- Running enrichment research across state license boards, PCAOB, SEC, OFAC, and specialty data providers

None of that work prices risk. All of it is required before risk can be priced.

The financial weight of that is significant. A mid-sized commercial carrier with 50 underwriters fully loaded at $75,000 per year is spending roughly $1.9 million annually on payroll going into work that AI agents now handle end to end. That is before you count the opportunity cost of lost submissions, slower broker response times, and underwriters who leave because the job is not what they signed up for.

The carriers winning the next decade are the ones treating this 50 percent as a fixable operational problem, not a permanent cost of doing business.

Four roles compound in value inside an AI-augmented commercial underwriting operation, and they are the roles commercial carriers and MGAs should be investing in between now and 2030.

1. Risk judgment specialists. The senior underwriters whose time flips from 50 percent admin to roughly 90 percent risk judgment. Their output goes up because the boring half of their day goes away, and they become the humans who teach the scoring model through described disagreement, correcting the AI when it misreads a risk and building institutional memory into the system.

2. Underwriting architects. The heads of underwriting operations and process excellence leads who calibrate risk factor weights, design the handoff between AI agents and human underwriters, and own the operating model for how a mixed human and AI team actually works. This is a brand new senior role that did not exist five years ago.

3. Portfolio strategists. The Chief Underwriting Officers and chief actuaries who own real-time portfolio intelligence, loss ratio accountability across the book, and the feedback loop between bound business and forward appetite. With AI handling submission intake, these leaders finally get the live portfolio visibility they have been asking analytics teams for across two decades.

4. Distribution relationship leaders. The broker-facing executives who turn speed advantages into durable broker loyalty. When submission response times drop from days to hours, brokers route their best business to the fastest, most consistent carrier. That is a relationship advantage that compounds.

Every other role in the pre-decision chain, submission intake clerks, data entry specialists, offshore BPO teams, routing coordinators, appetite checkers, and loss run parsers, is moving into the AI layer underneath the operation.

CEO and Founder, Pibit.AI

.png)

Ready to optimize